New report on the Missing Middles, with I&P’s contribution

Submitted by on Wed, 12/05/2018 - 10:11

Dalberg, the Dutch Good Growth Fund, Omidyar Network and the Collaborative for Frontier Finance published late October a report entitled “The Missing Middles: Segmenting Enterprises to Better Understand Their Financial Needs”, to which I&P provided data, expertise and guidance.

The report was presented at SOCAP in San Francisco and GIIN annual meeting in Paris through a series of presentations and workshops.

Discover the report →

Discover the report →

The context

According to the IFC, Small and Growing Businesses (SGBs) in emerging markets face a $930 billion financing gap. Many are stuck squarely in the “missing middle”: they are too big for microfinance, too small or risky for traditional bank lending, and lack the growth, return, and exit potential sought by venture capitalists.

SGBs are also incredibly diverse: ranging from an agricultural cooperative to a high-tech start up to an energy access venture serving base of the pyramid customers.

Objectives

The report aims to better understand and dissect this huge and diverse market – and identify the financing solutions that can be scaled up to address the distinct financing needs of different types of SGBs. It develops a segmentation framework with the aim of helping investors, intermediaries, and entrepreneurs better navigate the complex landscape of SGB investment in frontier and emerging markets.

By segmenting the SGB market into multiple “missing middles,” the report aims to help more effectively diagnose the distinct financing needs and gaps faced by different types of enterprises, and in turn better focus on scaling the financing solutions that are most needed to empower enterprises of all types to meaningfully contribute to inclusive economic growth.

Main findings

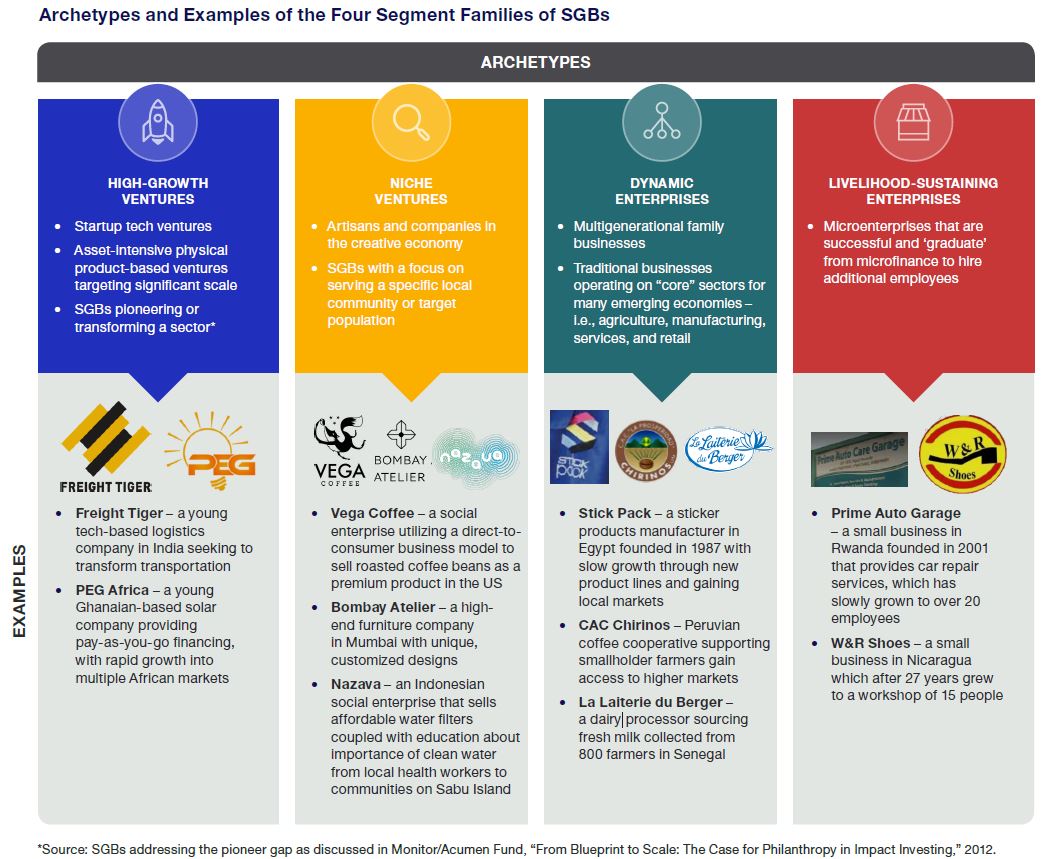

The report sorts SGBs with financing needs between $20,000 and $2 million into four distinct segments (‘’families’’), depending on their growth and scale potential, their innovation profile and the entrepreneur behavioral profile:

- High-growth ventures: disruptive business models with high growth and scale potential

- Niche ventures: create innovative products and services that target niche markets or customer segments whose total addressable market is limited

- Dynamic enterprises: medium sized enterprises that operate in established “bread and butter” industries (such as trading, manufacturing, retail and services) and deploy proven business models with steady but moderate rates of growth

- Livelihood-sustaining enterprises: opportunity-driven, family-run businesses that are on the path to incremental growth and serve highly local markets or value chains (may be local or informal)

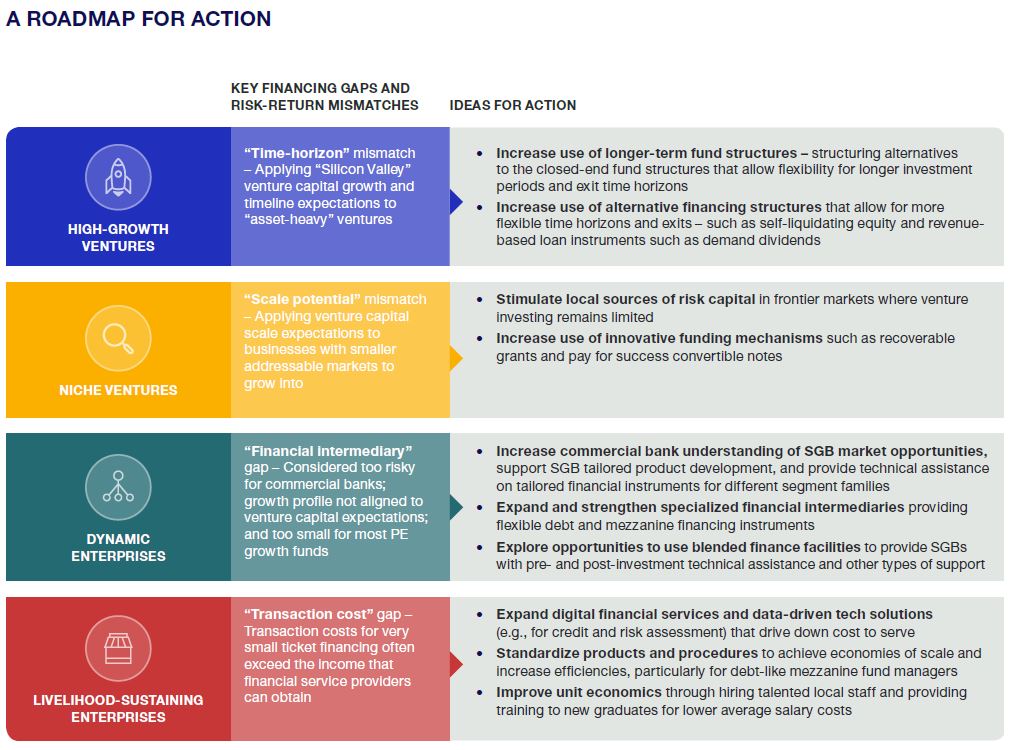

Each family has distinct financing needs, and faces different gaps or mismatches in the market between available investment options and the solutions that are best suited to enterprise needs.

I&P, through its funds IPAE and IPDEV 2, mostly targets two families identified by the report: dynamic enterprises and livelihood-sustaining enterprises. The funds IPAE 1 and IPAE 2, providing financing between €300,000 and €3 million, also include some venture SGBs.

- High-growth ventures: need staged “risk capital”. Certain types of High-growth Ventures—such as asset-light tech companies—are well served by conventional venture capital investing structures, with staged venture capital equity rounds. High-growth Tech Ventures are the segment of SGBs that are typically the best served by investors, particularly in economies where venture capital and private equity investing are established and growing.

- Niche ventures: like High-growth Ventures, often require risk capital early in their journey in the process of launching an innovative product or service. However, their capital requirements are often more modest in size.

- Dynamic enterprises: Dynamic Enterprises face significant financing gaps—in many ways, they are squarely “in the center of the missing middle.” Many of these businesses are well-established and large enough to have complex operations, and thus have financing needs distinct from those of startups. They can benefit from working capital solutions to meet short-term financing needs; lending that can enable capital expenditure for specific assets or investments that can fuel incremental growth; trade finance for relevant sub-segments; and, potentially, equity or equity-like capital to strengthen balance sheets and enable expansion opportunities. In many countries, very few financial service providers are focused on serving this large family of businesses. Many Dynamic Enterprises are simply not large enough or sufficiently high-yielding to justify the transaction costs or assuage the concerns of risk-averse commercial banks that prefer to serve larger businesses.

- Livelihood-sustaining enterprises: Livelihood-sustaining Enterprises have basic financial needs centered on short-term working capital. Critical constraints to financing Livelihood-sustaining Enterprises relate to transaction costs, the perceived risks of serving this segment family, and the challenges of cost effectively obtaining assessment data to be able to efficiently underwrite small-ticket-size loans.